AI-powered fraud prevention in digital payments has become essential as online transactions grow in volume and complexity. Consequently, financial fraud has evolved into a highly sophisticated and fast-moving threat. As a result, traditional rule-based fraud detection systems struggle to keep pace, often producing delayed responses or high false-decline rates.

To address these challenges, Mastercard has developed an advanced AI-powered fraud prevention ecosystem capable of analyzing transactions in real time at a global scale. In doing so, Mastercard’s fraud prevention systems leverage artificial intelligence and machine learning to evaluate billions of transactions using behavioral patterns, contextual signals, and adaptive risk models.

Moreover, by continuously learning from emerging fraud trends, these systems can identify suspicious activity within milliseconds—thereby reducing fraud losses while maintaining seamless customer experiences. This report therefore explores how Mastercard applies AI technologies to secure digital payments, the business and technical impact of these systems, and their role in shaping the future of payment security.

1. THE FRAUD LANDSCAPE: Understanding the Problem

The Current State of Card Fraud

The global payment fraud landscape is staggering. Currently, card fraud alone accounts for losses exceeding $30 billion annually worldwide. Furthermore, this figure continues to grow as e-commerce expands.

Meanwhile, fraudsters have evolved from simple card skimming to sophisticated operations. For example, modern attack methods now include:

Card-Not-Present (CNP) Fraud: This is the fastest-growing category, representing over 70% of all card fraud. With online shopping booming, criminals don’t need physical cards—just the card details.

Account Takeover Fraud: Criminals gain access to legitimate accounts through phishing, data breaches, or social engineering, then make unauthorized purchases.

Synthetic Identity Fraud: Fraudsters combine real and fake information to create new identities, open accounts, and build credit before maxing out cards and disappearing.

Friendly Fraud: Legitimate cardholders dispute valid charges, claiming they didn’t authorize them—a gray area that costs merchants billions.

Why Traditional Systems Fail

Old-school fraud detection relied on static rules. For instance, systems might block transactions over $1,000 in foreign countries. However, these rules created major limitations.

- First, they were easy for fraudsters to learn and bypass.

- Second, they generated massive false positives.

- Third, they could not adapt to new fraud patterns without manual programming.

- Finally, they were too slow for real-time commerce.

Therefore, traditional fraud detection could no longer meet modern payment security demands.

2. DECISION INTELLIGENCE: The Brain Behind the Operation

At the core of Mastercard’s fraud prevention strategy lies Decision Intelligence, a proprietary AI platform designed to operate at massive global scale. The platform is architected to evaluate complex transaction behavior in real time, balancing speed, accuracy, and adaptability.

Decision Intelligence relies on multi-layered neural network architectures that extract increasingly abstract signals from raw transaction data. Rather than relying on static rules, the system identifies non-linear relationships across hundreds of variables, enabling it to detect subtle fraud indicators that traditional systems often miss.

Key Architectural Components

- Multi-Layered Neural Networks

Deep learning models with multiple hidden layers analyze transaction data, progressively transforming raw inputs into high-level behavioral risk signals. - Real-Time Decision Processing

Each transaction is analyzed and scored in under 50 milliseconds, ensuring fraud checks do not impact customer experience.

The real-time pipeline includes: - Receiving the transaction request

- Retrieving relevant historical and contextual data

- Evaluating the transaction across multiple AI models

- Generating a risk score

- Returning an approve or decline decision instantly

The Data Universe Behind Each Transaction — Summary

- To accurately assess fraud risk in real time, Mastercard’s Decision Intelligence platform evaluates more than 500 distinct data points for every transaction. Rather than relying on isolated signals.

- At the transaction level, the system analyzes contextual details such as transaction amount, merchant category, location, time, and payment channel. These signals help establish whether a transaction aligns with expected usage patterns or deviates from normal behavior.

- Beyond user behavior, device intelligence adds another critical layer of protection. By evaluating device fingerprints, browser and operating system characteristics, and prior usage history, the system can detect anomalies such as unfamiliar or high-risk devices. This is further reinforced by network-level intelligence, which identifies broader fraud patterns across merchants, regions, and card populations.

The Learning Process

What truly differentiates Decision Intelligence is its continuous learning framework, which allows the system to evolve alongside fraud tactics. Instead of static detection logic, the platform adapts dynamically based on real-world outcomes and emerging patterns.

- Supervised Learning

Models are trained on billions of labeled transactions, learning to distinguish legitimate behavior from fraudulent activity with high precision. - Unsupervised Learning

The system autonomously detects anomalies and unknown fraud patterns, enabling early identification of new attack techniques. - Reinforcement Learning

Feedback from confirmed transaction outcomes refines decision boundaries, allowing the AI to self-correct and reduce false positives over time. - Transfer Learning

Insights gained from detecting one fraud pattern are applied to related scenarios, accelerating detection of new and evolving fraud schemes.

3. REAL-TIME FRAUD DETECTION: The Process Flow

Step-by-Step Transaction Analysis

Let’s walk through what happens when you make a purchase:

Step 1: Transaction Initiated (0-5 milliseconds)

You tap your card at a coffee shop. The terminal sends the transaction details to your bank (the issuer).

Step 2: Routing to Mastercard (5–10 milliseconds)

At this stage, the bank forwards the transaction through Mastercard’s network for authorization.

Step 3: Data Enrichment (10–20 milliseconds)

Next, Decision Intelligence instantly retrieves relevant context, including transaction history, device information, location data, and real-time merchant intelligence.

Step 4: AI Risk Scoring (20–40 milliseconds)

Meanwhile, multiple AI models run in parallel to analyze behavioral patterns, location consistency, transaction velocity, merchant reputation, and global fraud signals.

Model 1 – Behavioral Analysis: “This customer typically spends $3-8 at coffee shops on weekday mornings. This $5.50 transaction at 8:15 AM fits the pattern perfectly. Low risk.”

Model 2 – Location Intelligence: “Transaction is 2 miles from customer’s home address and where they’ve shopped before. Consistent. Low risk.”

Model 3 – Velocity Checking: “This is the first transaction today. No unusual purchasing velocity. Low risk.”

Model 4 – Merchant Analysis: “This merchant has clean history, no recent fraud spikes. Low risk.”

Model 5 – Global Pattern Matching: “No similar fraud patterns detected across network. Low risk.”

The system aggregates these model outputs into a single risk score from 0-999.

Step 5: Decision Making (40-45 milliseconds)

- Score 0-300: Auto-approve

- Score 301-700: Apply additional rules or request step-up authentication

- Score 701-999: Decline or flag for manual review

Step 6: Response Sent (45-50 milliseconds) The decision is sent back through the network to the merchant terminal.

Total time: Less than a human can perceive.

4. ADVANCED FEATURES AND CAPABILITIES

Behavioral Biometrics

Behavioral biometrics represents one of the most advanced layers of Mastercard’s fraud prevention strategy. Instead of relying solely on what a user knows (passwords) or what a user has (cards or devices), this approach focuses on how a user behaves. These behavioral patterns are extremely difficult for fraudsters to replicate, making them a powerful signal for detecting unauthorized activity in real time.

When a transaction occurs—especially in online or mobile environments—the system continuously observes subtle interaction patterns. These signals are analyzed passively in the background, without interrupting the user experience, to determine whether the behavior matches the genuine cardholder’s established profile.

Typing Patterns: The system evaluates how card details and other inputs are entered, including:

- Time gaps between keystrokes

- Overall typing rhythm and consistency

- Corrections, pauses, and hesitations

- Copy-paste behavior, which is common when fraudsters use stolen credentials

Device Interaction:On mobile and desktop devices, behavioral cues include:

- How the phone is held, using accelerometer and motion data

- Touch pressure, swipe speed, and gesture patterns

- Navigation flow through payment screens

- Mouse movement speed, angles, and pauses on computers

Session Behavior:The system also examines how a user interacts across an entire session:

- Time spent on each page

- Familiarity with the checkout process

- Consistency with previous sessions from the same account

- Sudden deviations from normal interaction patterns

If someone steals your card details but types completely differently than you do, the system notices.

Why Behavioral Biometrics Matters

Even if a fraudster obtains valid card details, their interaction behavior often differs significantly from that of the legitimate cardholder. By detecting these subtle inconsistencies—such as unnatural typing rhythms or unfamiliar navigation patterns—the system can flag suspicious transactions that might otherwise appear legitimate. This behavioral layer significantly improves fraud detection accuracy while reducing false declines and preserving a seamless checkout experience.

Network Intelligence and Threat Sharing

Network intelligence is one of the most powerful advantages of Mastercard’s fraud prevention ecosystem. By operating at a global network level, the system does not evaluate transactions in isolation; instead, it continuously learns from activity across millions of merchants, banks, and cardholders. This network effect allows emerging threats to be detected early and neutralized before they can scale.

A key capability of this approach is merchant compromise detection. When the system identifies a pattern where cards used at a specific merchant begin showing fraudulent activity elsewhere, it can infer a potential data breach—often before the merchant is even aware of the issue. This early detection enables rapid, coordinated response across the ecosystem.

How Network Intelligence Is Applied

- Merchant Compromise Detection

When suspicious patterns emerge, the system can:

- Alert the affected merchant

- Apply increased scrutiny to all transactions originating from that merchant

- Proactively notify potentially impacted cardholders

- Coordinate with issuing banks to reissue cards and limit exposure

- Fraud Wave Detection

New fraud techniques identified anywhere in the network are rapidly learned and shared. Once detected, protective measures are deployed globally within hours, not weeks—preventing widespread exploitation. - Cross-Border Intelligence

Fraud patterns that originate in one region are analyzed and flagged before spreading internationally. This enables early intervention and strengthens protection across borders and markets.

Why Network Intelligence Matters

By sharing intelligence across its global ecosystem, Mastercard transforms localized fraud incidents into network-wide learning opportunities. This collective defense model significantly reduces the impact of large-scale attacks while improving response speed, coordination, and overall payment security.

5. CASE STUDIES AND REAL-WORLD IMPACT

COVID-19 Pandemic Response

The COVID-19 pandemic created an unprecedented stress test for global fraud detection systems. Almost overnight, consumer spending behavior shifted in ways that traditional, rule-based models were not designed to handle. Patterns that had been reliable indicators of fraud for years suddenly became obsolete, increasing the risk of false declines and missed fraud across the payments ecosystem.

The Challenge

During the early stages of the pandemic, the payments landscape changed dramatically:

- In-store purchases dropped by 40–60% within weeks

- E-commerce and digital payments surged sharply

- Many consumers made large online purchases for the first time

- Entire spending categories shifted almost overnight

- Historical fraud patterns no longer reflected real behavior

For legacy fraud systems, these abrupt changes caused widespread disruption, as static rules could not adapt quickly enough.

Cryptocurrency and Gift Card Fraud

As fraud tactics evolve, criminals increasingly convert stolen card credentials into cryptocurrency and gift cards, which provide fast, hard-to-trace value. These channels present elevated risk because funds can be moved or resold almost instantly. To counter this, Mastercard’s Decision Intelligence platform applies targeted AI models designed specifically for these high-risk transaction types.

How Decision Intelligence Detects This Fraud

The system relies heavily on pattern recognition, learning behavioral sequences that commonly indicate misuse rather than isolated transactions. For example, the AI has learned to flag scenarios such as:

- Multiple failed attempts to purchase cryptocurrency followed by a sudden successful high-value transaction

- Large gift card purchases made with unfamiliar merchants

- Rapid sequences of gift card purchases across multiple retailers

These behavioral patterns often signal attempts to quickly convert stolen card data into liquid assets before detection.

Merchant-Specific Risk Modeling

Decision Intelligence also applies customized risk models for cryptocurrency exchanges and gift card merchants. Unlike general retail transactions, these categories require specialized analysis that accounts for:

- Sudden changes in purchase value

- First-time interactions with high-risk merchants

- Cross-merchant purchasing behavior within short timeframes

Why This Matters

By combining behavioral sequencing with merchant-specific intelligence, Mastercard can detect and block fraud attempts at the conversion stage—where financial loss becomes difficult to recover. This targeted approach reduces exposure to emerging fraud vectors while allowing legitimate crypto and gift card purchases to proceed with minimal friction.

6. INTEGRATION WITH BROADER ECOSYSTEM

Merchant Protection

Fraud prevention is not only about safeguarding cardholders—merchants also absorb billions in losses each year due to fraudulent transactions and chargebacks. Therefore, Mastercard’s AI-driven fraud intelligence helps reduce these losses by preventing high-risk transactions before they are completed. As a result, by lowering the number of fraudulent purchases, merchants can avoid costly chargebacks where both the product and the payment are often lost.

In addition to prevention, the system enables real-time decisioning at the point of sale. As a result, merchants receive instant risk assessments that allow them to apply additional verification—such as signatures or step-up authentication—only when necessary, while keeping low-risk transactions fast and frictionless. Beyond individual transactions, aggregated fraud insights give merchants visibility into their overall risk profile. In turn, this helps them identify vulnerabilities, adjust security controls, and implement more effective fraud mitigation strategies over time.

Consumer Experience

From the cardholder’s perspective, Mastercard’s AI-driven fraud protection is designed to be almost invisible—and that is intentional. Therefore, the system focuses on keeping legitimate transactions seamless while quietly working in the background to stop fraud before it causes disruption. As a result, more than 99% of genuine transactions are approved instantly, without requiring any additional action from the customer.

When a transaction does require further verification, the authentication process is designed to be intelligent and minimally disruptive. Instead of forcing cardholders to call their bank or abandon a purchase, the system typically uses convenient methods such as one-time passcodes sent via text message. In parallel, many cardholders benefit from proactive real-time alerts, allowing them to quickly confirm or report suspicious activity. By significantly reducing false declines, the AI also eliminates frustrating and embarrassing checkout interruptions, creating a smoother and more trusted payment experience overall.

7. THE FUTURE: What’s Next for AI Fraud Prevention

Biometric Authentication Integration

The future of secure payments is increasingly biometric-driven, shifting authentication from static credentials to natural human characteristics. Mastercard is moving toward integrating biometrics as a core layer of payment security, enabling authentication that is both stronger and more seamless for users.

Key biometric directions include:

- Fingerprint and face recognition as standard payment authentication on mobile devices

- Behavioral biometrics at scale, enabling continuous, passive authentication based on user interaction patterns

- Voice authentication for phone-based and virtual assistant transactions

- Heartbeat and pulse pattern analysis, an emerging biometric signal under active research

This evolution aims to make payments more secure while reducing friction for cardholders.

Predictive Fraud Prevention

Fraud prevention is shifting from reactive detection to proactive prediction, enabling risks to be addressed before financial damage occurs. Mastercard is advancing toward predictive fraud models that identify threats early, often before a fraudulent transaction is even attempted.

Key predictive capabilities include:

-

First, pre-transaction risk assessment scores accounts and behaviors for fraud likelihood in advance, rather than only at the point of transaction.

-

Next, early warning systems detect subtle anomalies that signal merchant compromise before fraud spreads.

-

Meanwhile, synthetic identity detection at onboarding identifies fake or manipulated identities during account creation instead of after losses occur.

As a result, by acting earlier in the fraud lifecycle, predictive models reduce financial impact while improving trust and system resilience.

8. COMPETITIVE LANDSCAPE

How Mastercard Compares

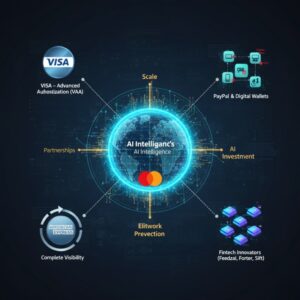

Visa’s Advanced Authorization (VAA): Similar AI-driven approach, with comparable results. The competition drives innovation.

American Express: Known for sophisticated fraud detection, partly because they’re both issuer and network, giving them complete data visibility.

PayPal and Digital Wallets: These have advantages (more contextual data about devices and accounts) and disadvantages (higher fraud rates for new payment methods).

Fintech Innovation: Startups like Feedzai, Forter, and Sift are pushing the boundaries with specialized fraud detection SaaS platforms.

Mastercard’s Competitive Advantages

Scale: Processing data from billions of transactions globally provides unmatched training data.

Network Position: Sitting between issuers and merchants gives unique visibility into both sides of transactions.

Investment: Billions invested in AI research and infrastructure.

Partnerships: Collaborations with leading AI research institutions and technology companies.

CONCLUSION: The Ongoing Evolution

Mastercard’s AI-powered fraud prevention represents one of the most sophisticated practical applications of artificial intelligence in the world today. With Decision Intelligence processing billions of transactions yearly, the system must be:

- Accurate enough to catch sophisticated fraud

- Smart enough to minimize false positives

- Adaptive enough to handle changing behaviors and new threats

- Scalable enough for global operations

- Secure enough to protect sensitive data

The system succeeds on all these dimensions, demonstrating how AI can solve complex, high-stakes problems at massive scale.

As fraud tactics evolve and payment methods proliferate, the AI will continue advancing. In reality, fraud can’t be eliminated. However, it can be made so difficult and unprofitable that criminals simply move on to easier targets.

For consumers and merchants, this means greater security without sacrificing convenience. For the payments industry, it represents a critical competitive advantage and a demonstration of responsible AI deployment. The future of payments is intelligent, adaptive, and secure—and Mastercard’s AI is leading the way.

Know more relevant topics:

The “Tetris” Paradox: Why Nature is Better at Packing than Math:

The “Tetris” Paradox: Why Nature is Better at Packing than Math